External OEM storage revenue rises 3.9% to USD $33bn

Thu, 12th Mar 2026

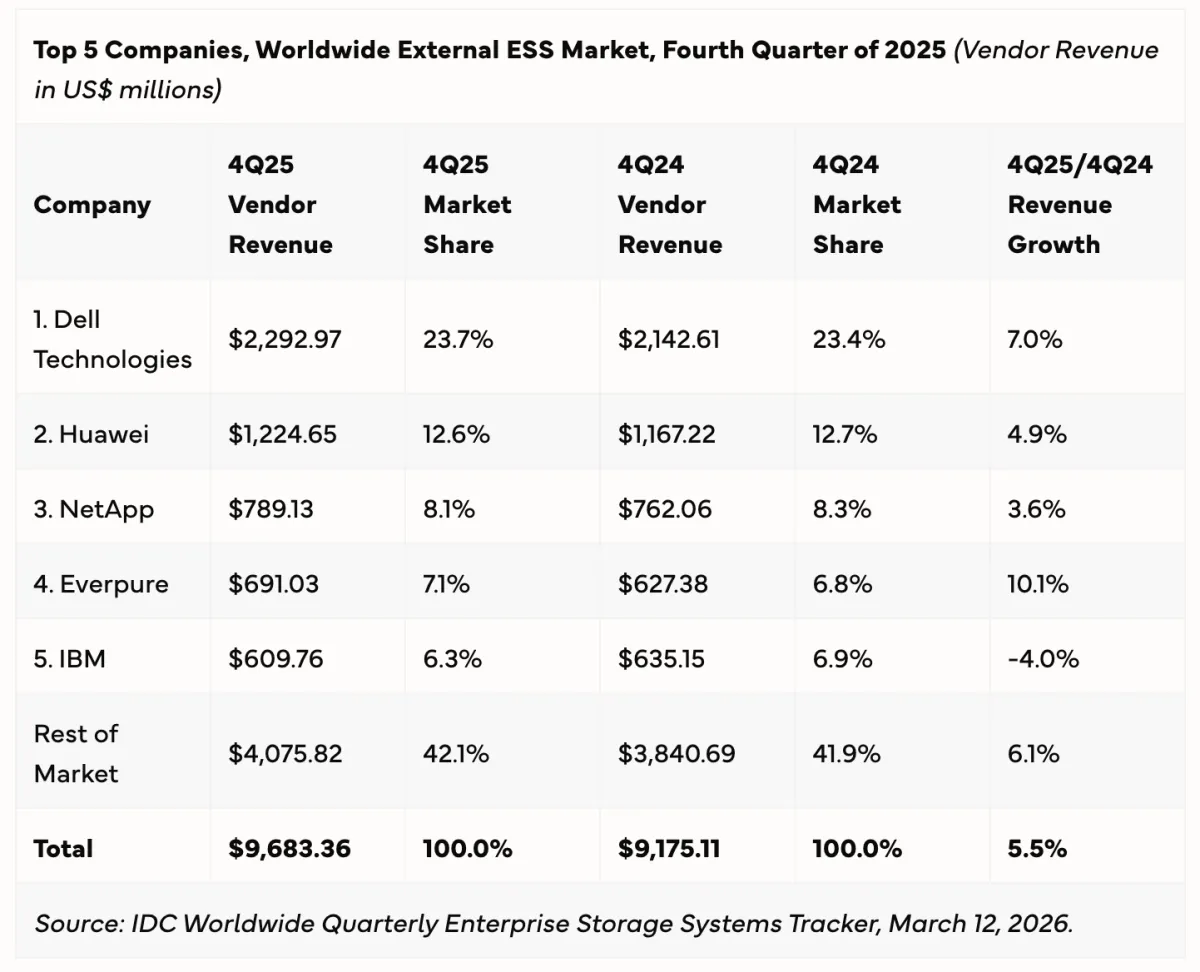

Worldwide revenue in the external OEM enterprise storage systems market rose 3.9% in 2025 to USD $33.0 billion, according to IDC. Fourth-quarter revenue reached USD $9.7 billion.

In the final quarter, the market grew 5.5% year on year as spending picked up after companies delayed storage infrastructure refresh cycles. That growth came despite broader attention on stronger gains in servers.

Product trends were mixed across storage formats. Revenue from all-flash arrays increased 18.1% from a year earlier, while hard disk drive arrays returned to growth with a 3.1% rise. Hybrid flash arrays moved the other way, falling 6.7%.

IDC also broke out demand by price band. Midrange systems, defined as those with an average selling price of USD $25,000 to USD $250,000, expanded 8.5% and accounted for 66% of the external storage market. High-end systems priced above USD $250,000 rose 5.4%, while entry-level systems below USD $25,000 declined 6.9%.

The figures point to a market in which buyers are still spending but shifting budgets across equipment categories. Component shortages have supported higher values, with capacity proportional value, measured in dollars per gigabyte, up 5.5% from the same quarter a year earlier.

Price changes in SSDs, HDDs and DRAM also shaped buying patterns. The data showed that some companies moved to secure shipments early over concerns about further increases, while others opted for a mix that included HDD-based platforms to keep costs under control.

Regional split

Most regions recorded growth in the quarter, although performance varied. The PRC and the US outpaced the market average, with revenue growth of 8.0% and 6.9%, respectively.

EMEA increased 4.3% and Latin America rose 1.8%, both below the overall rate. Japan was nearly flat at 0.8%, while Asia Pacific excluding Japan and China slipped 0.1% and Canada declined 0.8%.

Vendor rankings

Dell Technologies remained the largest supplier, with a 23.7% revenue share, gaining 0.3 percentage points during the period.

Huawei ranked second with a 12.6% share, helped by strong results in the PRC market. NetApp was third with 8.1%, driven by its performance in all-flash arrays.

Everpure took fourth place with a 7.1% share after recording double-digit quarterly growth. IBM rounded out the top five with a 6.3% market share.

The quarterly results suggest delayed replacement cycles are now feeding through to storage spending, even as subdued economic growth and geopolitical tensions continue to weigh on corporate planning. IDC said those pressures remain the market's main concern.

Juan Seminara, Research Director, Worldwide Enterprise Infrastructure Trackers, said buyers are balancing several spending priorities as they respond to changing component costs and ageing infrastructure.

"Storage demand would navigate between a continued increase on components prices and the growing infrastructure refreshing needs from companies of all sizes, we might see a positive 2026 for the market with end users trying to balance their CAPEX between hardware, software, management efficiency and as a service models in order to meet their needs," Seminara said.